|

https://twitter.com/RealEstateLand3/status/1620362281300414465

— Real-Estate Land Development Limited (@RealEstateLand3) January 31, 2023https://twitter.com/RealEstateLand3/status/1538517664615768065 https://twitter.com/RealEstateLand3/status/1620362954335223808 https://twitter.com/RealEstateLand3/status/1620364323385389056 https://twitter.com/RealEstateLand3/status/1620365702610972672

0 Comments

Chatgpt, AI and the Affordable Housing Crisis https://openai.com/blog/chatgpt/[/caption] https://openai.com/blog/chatgpt/[/caption]

Affordable Housing Crisis solutions ?

There are several potential solutions to the affordable housing crisis, including:

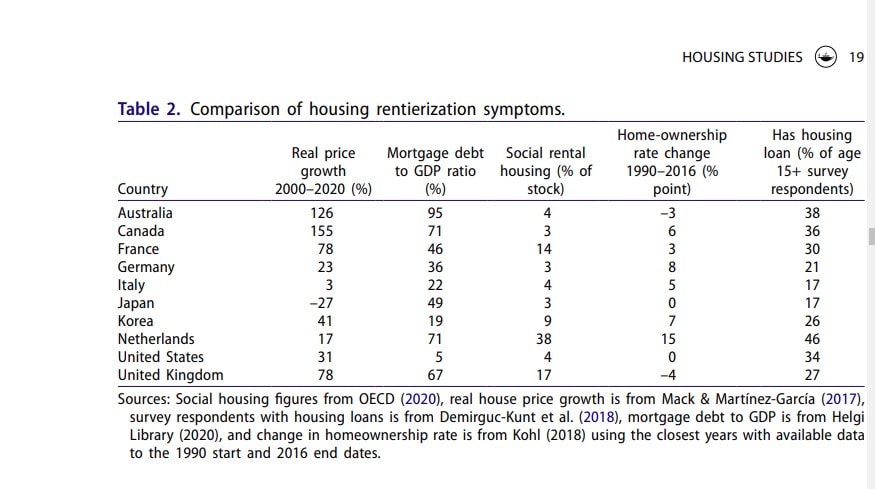

Home ownership rates and Affordable Homes, The Housing Ladder?

Homeownership rates refer to the percentage of households that own their own homes, as opposed to renting. The housing ladder is a term used to describe the process of moving up from renting to homeownership. Homeownership rates have traditionally been seen as a measure of economic stability and upward mobility, as owning a home is often considered a key step on the "housing ladder." However, homeownership can also be a source of financial stress, particularly for low-income households. The affordability of homes is a key factor in determining homeownership rates, as many low-income households are unable to afford to purchase a home. The lack of affordable homes can make it difficult for households to move up the housing ladder, as they may not be able to afford to purchase a home even after saving for a down payment. In recent years, the affordable housing crisis has led to a decrease in homeownership rates, particularly among low-income households. This is due to a number of factors, including rising housing costs, stagnant wages, and a lack of affordable housing options. To address the affordable housing crisis, there are a number of policy solutions that can be implemented to increase the supply of affordable homes and improve access to homeownership for low-income households. These include increasing funding for affordable housing development, implementing inclusionary zoning policies, and reducing barriers to housing development. Additionally, providing financial assistance and education to help low-income households purchase homes, can help to improve the housing ladder.

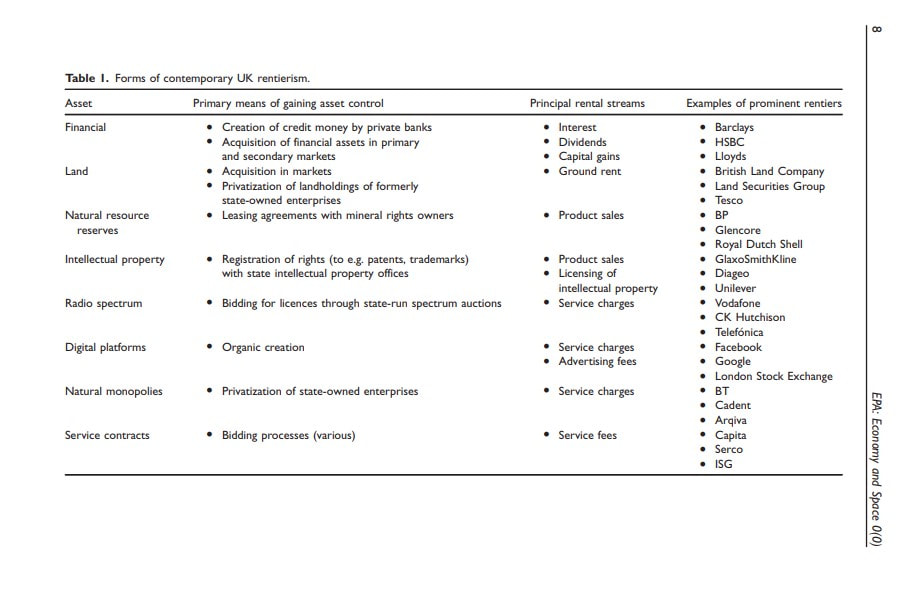

Absorption rates for new home development and Rentierisation and Financialisation of the Finance and Housebuiding sectors?

Absorption rate for new home development refers to the rate at which new homes are sold or rented. It is calculated by dividing the number of new homes sold or rented in a given period by the total number of new homes available during that period. A high absorption rate indicates that there is a strong demand for new homes, while a low absorption rate suggests that there is an oversupply of new homes on the market. The Rentierisation and Financialisation of the finance and housebuilding sectors refers to the increasing trend of large financial institutions and real estate companies becoming involved in the housing market. This trend has led to the commodification of housing, with homes becoming increasingly viewed as financial assets to be bought and sold for profit rather than places to live. This trend has led to a number of negative consequences, including the displacement of residents and the exacerbation of the affordable housing crisis. Additionally, when the housing market becomes dominated by financial institutions and real estate companies, the development and management of housing is often driven by financial considerations rather than social and community needs. To address the negative effects of the rentierisation and financialisation of the housing market, policymakers can implement a number of measures, including increasing regulation of the real estate market, providing incentives for the development of affordable housing, and encouraging community ownership of housing. Additionally, promoting financial education and regulations to make sure that it is not just a way of speculation but a way of encouraging citizens to have a sustainable future.

Big Bang and Liberalisation and the effect of neo liberal ideology on supply side measures rather than systemic fiscal and monetary demand side policies

The Big Bang refers to a series of financial market deregulation measures that were implemented in the UK in 1986. These measures, which included the deregulation of stockbroker commissions and the removal of fixed commissions for securities trading, aimed to increase competition and efficiency in the financial markets. Liberalization is a term used to describe the process of removing government regulations and restrictions on economic activity. Neo-liberal ideology is a political and economic philosophy that emphasizes free markets and minimal government intervention in the economy. The effect of neo-liberal ideology on the housing market has been to focus on supply-side measures, such as deregulation and privatization, rather than on systemic fiscal and monetary demand-side policies. This has led to an emphasis on increasing the supply of housing through private sector development, rather than on addressing the underlying demand for affordable housing through policies such as rent control, public housing construction, and subsidies. The adoption of neo-liberal policies has led to a decline in the availability and affordability of housing for low-income households, and has contributed to the financialization of housing. There has been a growing criticism of this ideology, arguing that it has led to the creation of a housing market that prioritizes the interests of developers and investors over those of renters and buyers, and that it has failed to address the underlying issues causing the housing crisis. To address the negative effects of neo-liberal policies on the housing market, some experts suggest a shift towards demand-side policies, such as increasing subsidies for low-income renters and implementing policies to increase access to affordable housing, as well as addressing the systemic issues such as lack of affordable financing and lack of regulations on the financial sector that is driving the financialization of housing.

Monoplisation,Rentierisation and Financialisation.

|

AuthorRoger Lewis, CEO of Home@ix writes this Blog, and the opinions expressed are his alone. Archives

July 2023

Categories |

Aadhaar and the post 2008 Looting? Buzz Feed Article The Dash For Cash.[/caption]

Aadhaar and the post 2008 Looting? Buzz Feed Article The Dash For Cash.[/caption]

RSS Feed

RSS Feed