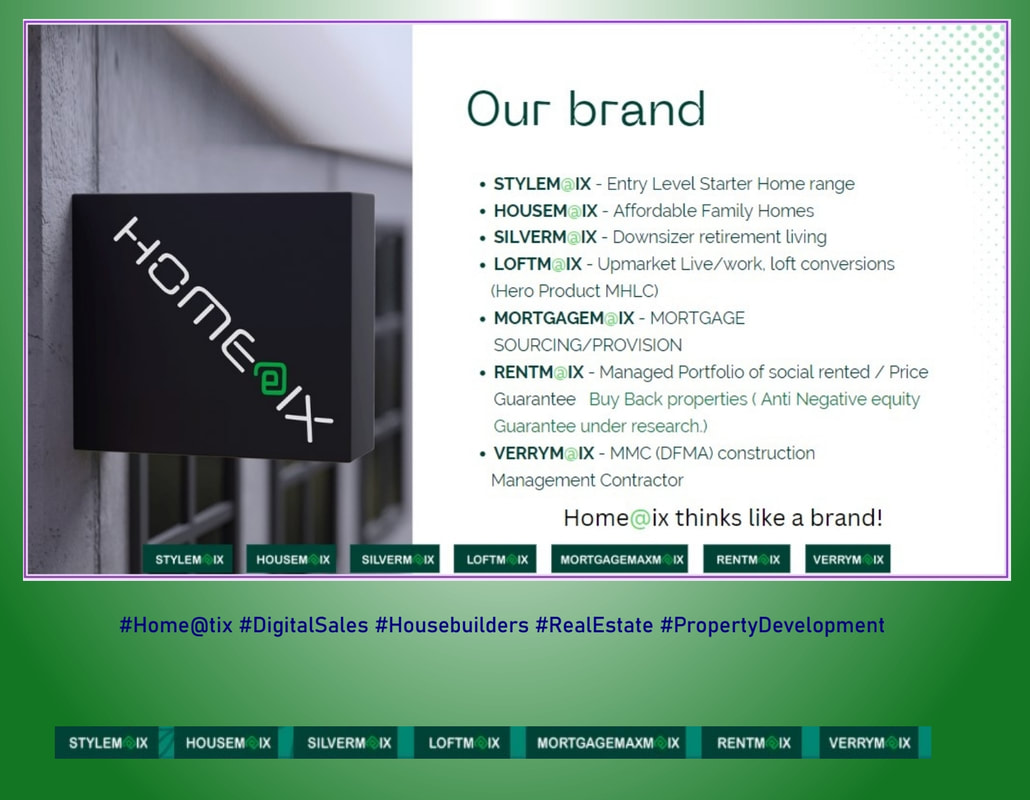

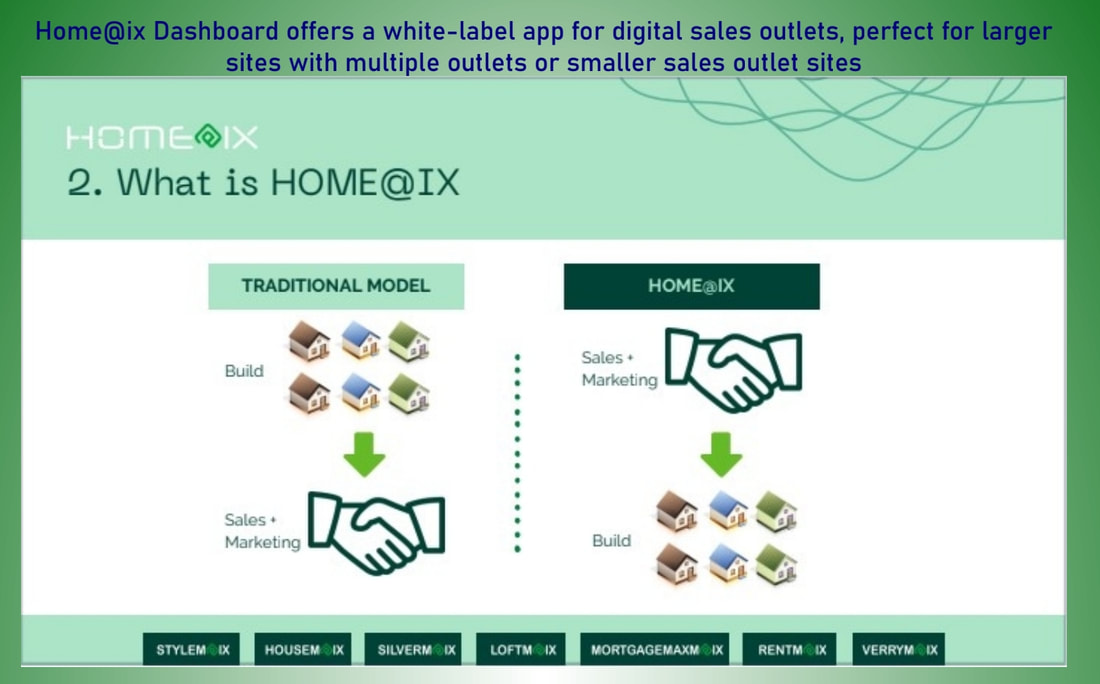

HOME@IX OFFERS DIGITAL SALES OUTLET DASHBOARD

Home@ix Dashboard for Volume House builders.

The Home@ix App can be white labelled as an additional Digital Sales outlet on existing larger sites with Multiple outlets or on Smaller sales outlet sites. It offers the opportunity to satisfy Conditionality in s.106 and CIL provisions for, Down-sizers, sheltered/assisted/Care-home, Key worker and Live-work buyers or renters for Housing association and PRS (Fleet Buyers) and for off BIM sales to targeted local demand home owner-groups specific to a particular location. Digital Sales outlets do not have the attendant absorption rate or Work in progress (WIP) cost calculation requirements and are complementary to and additional to existing sales and marketing and Sales per outlet projections.

As a House builder Our current focus is on the Downsizer and retirement end of the market and we are

actively pursuing smaller schemes for 5 to 35 homes in England and Wales. Phasing has become a large factor especially with respect to absorption rates and we have been exploring deferred land payment deal structures with other Land owners. #Home@tix #DigitalSales #Housebuilders #RealEstate #PropertyDevelopment

What is strategic land? Option and promotion agreements.

●Conditional contract: This is a contract of sale of land where the sale is conditional on the buyer first obtaining, at its own cost, planning permission. ●Land assembly: Where a developer brings together smaller areas of land, buying the land or using landowners agreements or options, which are then merged together to create a viable larger scheme. ●Option agreement: The developer has the option within an agreed time period to purchase the land from the landowner, the option permits or requires the developer to secure planning permission to generate the enhanced purchase price. ●Promotion agreement: The promoter agrees to promote the site and obtain either an allocation or planning permission. The landowner then sells the land, paying the promoter a fee.

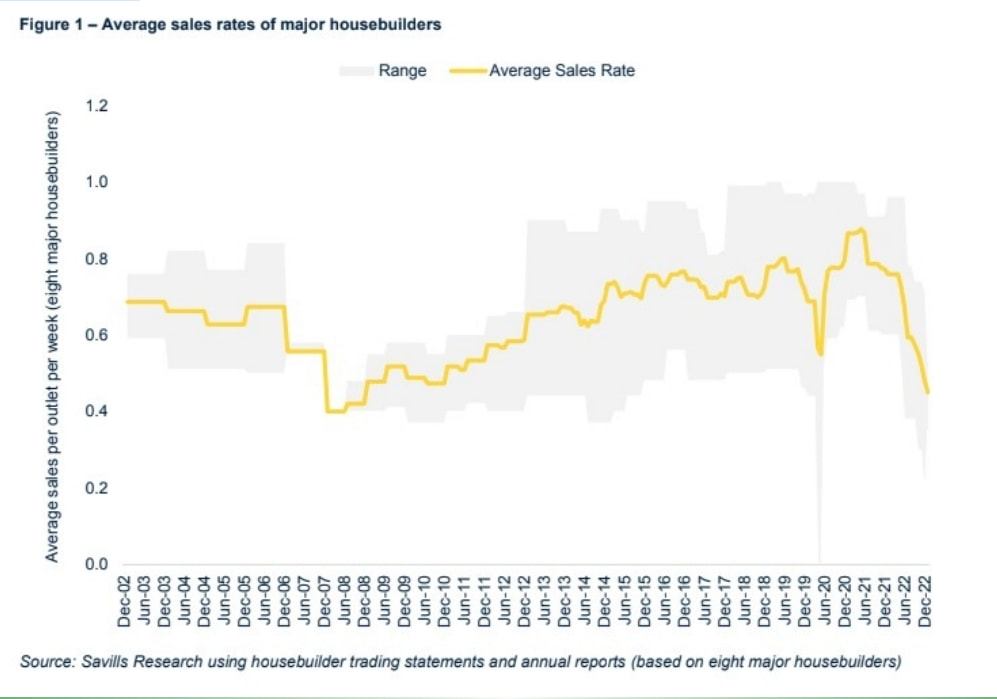

Bellway Sales rate per outlet 0.58 Since February..

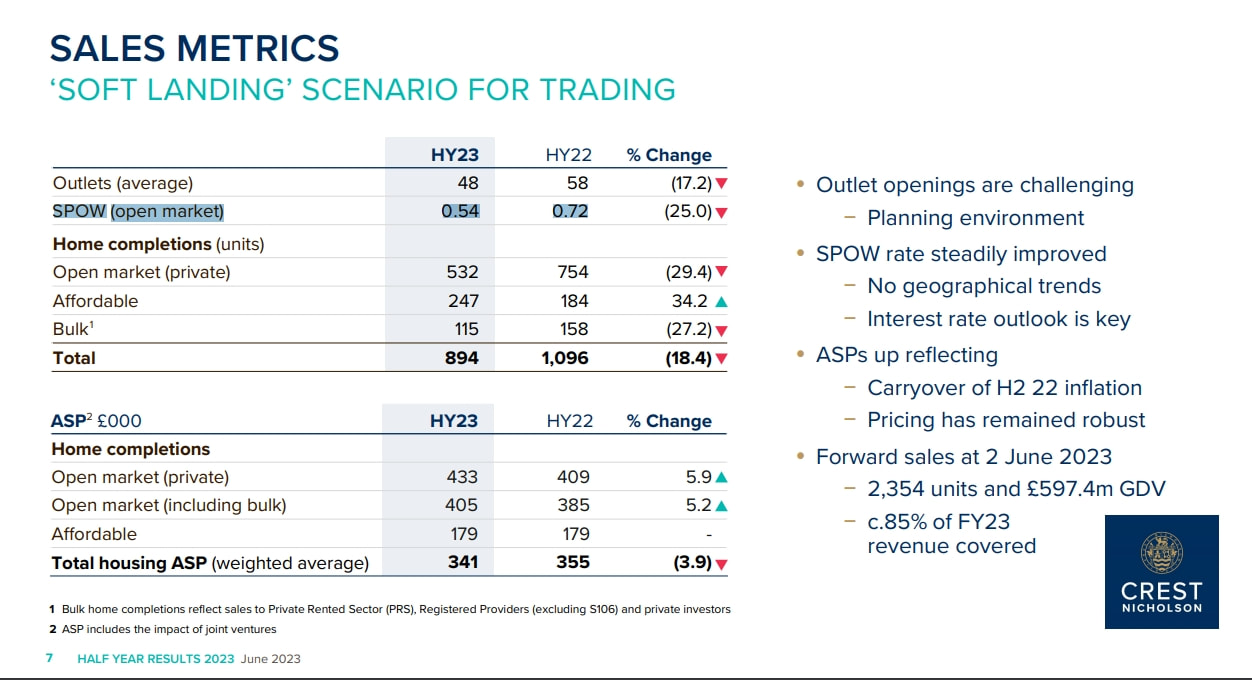

In Line with Crest Nicolson SPOW (open market) 0.54 hy 2023 0.72 hy 2022

Home@ix Slide Presentation New by Real-Estate Land Development Limited

The importance of sales outlets in a market without Help to Buy. (Dec 22-

March 2023) Executive Summary The housing market has experienced a significant shift in demand and sales rates as a result of the end of Help to Buy and the Covid-19 pandemic and Bank of England Interest rate rises. The number of sales per outlet per week has decreased, and the number of sites gaining planning consent has fallen by 31% over the last five years. This has made it difficult for house builders to open more outlets and deliver the Government's target of 300,000 new homes per year. This trend, will not reverse until local planning authorities and House builders work together to increase the number of sites gaining planning consent, “allowing house builders to open more outlets and provide a diverse range of products, locations, and price points”. The National Planning Policy Framework (NPPF) needs to support this by delivering consents for the right number and range of sites, including smaller sites that support SME house builders and new entrants into the industry. By doing so, the housing market can improve choice for buyers and contribute to an overall increase in new homes delivery. Sales Rates The housing market in England is heavily reliant on sales of new homes to owner occupiers, which take place in sales outlets on new homes development sites. The number of sales per outlet per week had increased from 2012 to 2019 supporting increased housing delivery despite a relatively static number of outlets. However, recent mortgage market turmoil and falling demand in the housing market, coinciding with the withdrawal of Help to Buy, has had a dramatic effect on sales rates, which fell to an average of 0.45 at the end of 2022, a level not seen since the Global Financial Crisis. Analysis from Savills suggests that sales rates per outlet are likely to remain at between 0.5 and 0.6 over coming years, with the lower end of this range persisting until housing market conditions stabilise. “The higher end of the range is likely to be reliant on the success of replacement schemes for Help to Buy, particularly Deposit Unlock. Without Help to Buy or a replacement scheme, we expect sales rates to be lower than the pre-GFC period in line with wider housing market activity levels”. Major housebuilder sales rates and delivery The sales rates and delivery of major housebuilders are crucial metrics in the housebuilding industry. Sales rate is defined as the average number of homes sold by a developer across each outlet on a weekly basis. Data reported by Savills; “shows that the average sales rate per outlet among major housebuilders was around 0.62 to 0.68 between 2003 and 2007, before falling sharply during the Global Financial Crisis to hit a low of 0.40 in 2008. Since then, the average sales rate has gradually increased, reaching a stable level of approximately 0.73 between 2015 and 2019.”

However, sales rates fell during the first Covid lockdown before rising to an average of nearly 0.87

during 2021 and 2022. Although some major housebuilders have reported results for the beginning of 2023, they remain lower than the previous two years. It is important to note that while the publication of sales rates has become common practice, it is not compulsory, which means reported figures may be biased towards housebuilders with better results. Crest Nicholson at 0.35 for the eleven weeks since November 1st 2022, Vistry Group a rate of 0.46 in Q4 2022 (compared to 0.84 in H1 2022) and Barratt at 0.44 across H2 2022 (down from 0.79 in H2 2021). Redrow reported 0.51 for the first five weeks of the year and Persimmon reported 0.52 for the first eight weeks (up from 0.3 in Q4 2022 but down from 0.96 for the same period of 2022).

Land Supply and Outlets

The number of outlets for housing has reached its lowest level in at least 20 years, with a continuing downward trend as the number of sites gaining planning consent has fallen every year since 2017. While the number of plots gaining consent declined less, over the last three years, with a 31% decrease in consented sites compared to a 15% decrease in consented plots plainly, Sites gaining consents are Larger. The lack of new sites, particularly smaller ones, gaining planning consent is a symptom of SME housebuilder decline and continuing barriers to entry for new entrants into the housebuilding industry. Measures That can increase land supply and outlets to meet the growing demand for housing should be welcomed.

Impact on delivery and What needs to change.

Delivery. The sales rate has fallen to levels not seen since the Global Financial Crisis, resulting in a decrease in new home completions. Even if the number of outlets remained constant, a sales rate of 0.5 would reduce the number of new homes sales from 145,000 to 90,000. This would make it impossible for the government to reach its target of delivering 300,000 new homes per year. To address this issue, local planning authorities need to recognise the changed market conditions and include more sites in housing trajectories to maintain and increase delivery. The National Planning Policy Framework needs to support this by delivering consents for the right number and range of sites, catering to a diverse range of developer types, including SME house builders. Although government policy has attempted to increase the number of SME house builders, the availability of smaller sites has only worsened in recent years. However, there is an opportunity for the planning system to deliver more smaller sites and lift a significant barrier to growth for SME house builders. Overall, changes are needed to support the housing market and appeal to a wider range of buyers through product, location, and price point.

Please call Roger Lewis for details of our Digital Sales Outlet Dashboard

0 Comments

Leave a Reply. |

AuthorRoger Lewis, CEO of Home@ix writes this Blog, and the opinions expressed are his alone. Archives

July 2023

Categories |

RSS Feed

RSS Feed